|

Sept

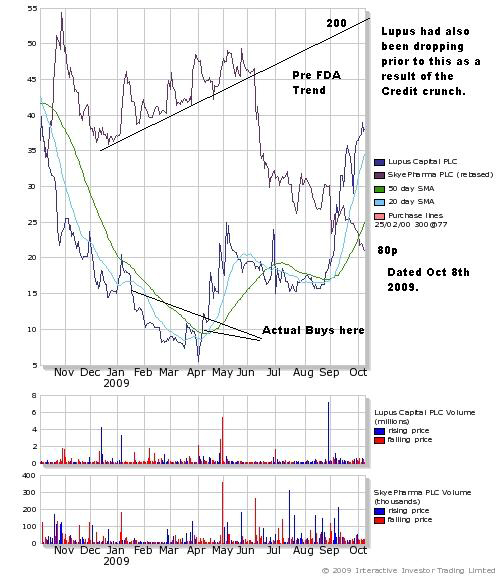

9th 100,000 buy today and 80,000 buy! |

|

This page is

written taking the company as a new investment from the time of the

Open Offer Sept. 2008. The share capital has been restructured, with

split shares cancelled before the consolidation, so there is little

point going over past history by referring to shares at "almost

Two Hundred Pounds each" by back converting without considering

that. Indeed the Stock Market disclaimer over performance states just

that! Past performance etc! The board has been criticised for past

action, but renegotiating the bonds was successful and the Open Offer

very timely indeed - and it was well received too! Also cash has been

recovered over the Certihaler content failure. That may be too late

to appear on the results and also had a major material effect on the

last results which already were very positive - see below.

Regrettably, unspecified new demands from the FDA have produced a

major slide, which looks to be rather over done! |

|

The shares

soared under the Tech boom, but drifted back - (see

this page dated 2003). Many investors from that period who did

not "stop loss" out were 90% and more down. The recent

offer (at1.5p OLD [10p] shares - now 150p [100p]) gave (IMHO) at

least a chance to redeem some of those losses, (170 shares for every

100). In the days after trading in the new shares began (as the

trading began to settle) they could have been bought for 130p. There

have been opportunities to "trade" the shares at profit

since then. Stop losses should have triggered in June, though the

drop was totally unexpected as a result of another possible new FDA request! |

|

Previous

analysis prior to the June slide appears here - for reference. |

|

SKYEPHARMA PLC - Settlement of Formoterol Certihaler™ Termination

LONDON, UK, 17 July 2009 - SkyePharma PLC (LSE: SKP) today

announces that it has reached agreement with Novartis Pharma AG

("Novartis") and with a subcontractor on immediate

termination of the contracts relating to formoterol Certihaler™.

The agreements follow the decision not to proceed with US

commercialisation of formoterol Certihaler™ as announced in

December 2008.

The net effect of the termination agreements

will result in an exceptional gain to SkyePharma in the 2009 accounts

of approximately £5 million leading to a net cash benefit in the

second half of 2009 of a similar amount. The

cessation of production resulted in a £5.9 million exceptional

charge in the Group's 2008 accounts mainly relating to asset write-downs.

Following the termination, SkyePharma retains exclusive rights for

the SkyeHaler™ device, used in the formoterol Certihaler™,

which was approved in the United States in December 2006 for use as a

multi-dose dry powder inhaler.

As previously announced, discussions on commercialising formoterol

Certihaler™ with a third party ceased following recommendations

by the Joint Advisory Committees of the US Food and Drug

Administration ("FDA") that the benefits

of long-acting beta2-agonists administered alone did not outweigh the

risks in current asthma indications.

SkyePharma is seeking other potential applications for its

proprietary SkyeHaler™ dry powder inhaler. SkyeHaler™ is a

multi-dose reservoir device suitable for acute and chronic therapies

with a dose counter and an end of life lock out mechanism.

Dr Ken Cunningham, Chief Executive, said: "It was

disappointing that formoterol Certihaler™ could not be

commercialised, but we are pleased to have reached

a settlement which includes a substantial cash receipt as well as enabling

us to seek alternative uses for

the SkyeHaler™ device, which remains one of very few dry powder

inhaler devices which have been incorporated in an approved product

in the United States." |

|

At iii it has now been admitted that the inhaler could not be

offered for other uses until this agreement, as I had already stated!

It appears to me that the cash element is in compensation for this.

The original cessation of production impacted on the results for that

half (2008) and the cash element announced above will be a post

balance sheet item this time (August 21st). (I confirmed this with

the company today) Mr Smith has not removed the  s on my correct posts on the matter and has STILL not posted!

s on my correct posts on the matter and has STILL not posted! |

|

There was also a mention of "distressed bondholders".

Are these the same people converting those bonds at £3.17 a go? The

total amount of the £69.6m 6% 2024 Convertible Bonds now

converted amounts to £6,587,000 saving £395,220 interest

per annum. They do not appear to be

selling the shares! |

|

This is the type of response the news above gets from a

contributor at iii! (spelling as original) |

|

Patrick,

Whatever the results, this now has to make a gain of nearly 30% to

get to its consolodation level.

And todays news is in fact another failure,

maybe not directly attributed to the board of directors, but in

general a failure and they still pick up nearly 6 million quid.

I can see the plans now to lay more of the workforce off because

of the news today (er

why exactly?) ,start another couple of directors on top whack

and have a cracking Xmas party planned

Oh to be a director of Skyepharma |

|

How is it a failure, to recover that amount of cash, when it was

the content of the inhaler, not the inhaler itself which

caused the original cancellation. Something which could NOT be anticipated!

The way director remuneration is calculated can be seen on the

website. It is not unusual! |

|

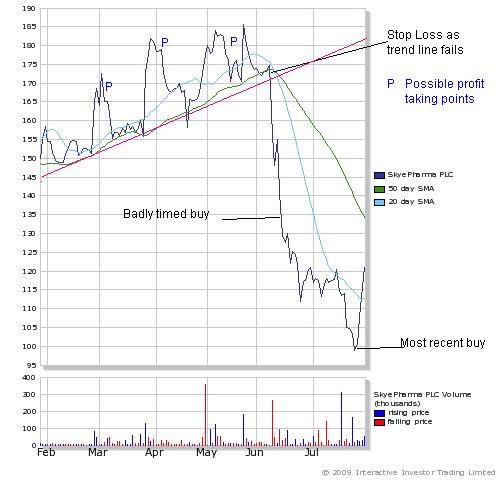

June 9th.2009.

It seems the FDA may want yet more information - Cancelled out

all the 2009 price rise in 2 days! Why they cannot get their

requirements right first time is puzzling! They have now done this TWICE!

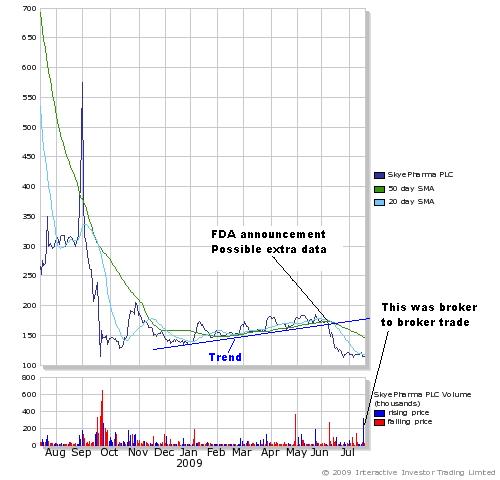

This testing has been going on since 2007 now! The chart below (Dated

June 17th) shows the drastic effect on the share price. NB the

announcement was "MAY" require more data. Should this not

be the case, or the data not require a long process, then the uptrend

shown on the chart could be resumed very quickly! A second, more

recent chart appears below this one. |

|

|

|

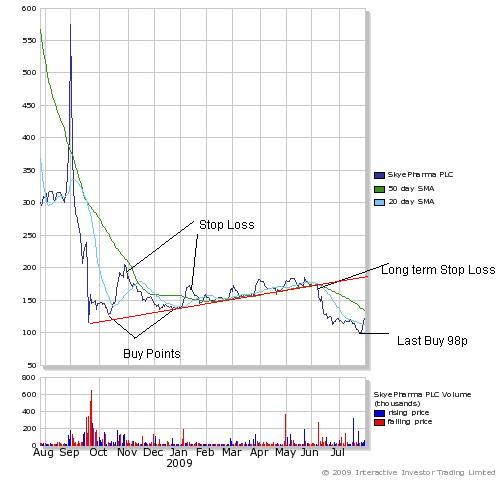

July 28th. Chart below shows breach of 20 day moving average and

two Gaps up! |

|

|

|

|

|

RNS Number : 6153T Skyepharma PLC 09 June 2009

SKYEPHARMA PLC - Flutiform* U.S. Filing Update

LONDON, UK, 9 June 2009 - SkyePharma PLC (LSE: SKP) today

announces that the US Food and Drug Administration (FDA) has issued a

communication in respect of the New Drug Application (NDA) for its

lead development product, Flutiform* (fluticasone

propionate/formoterol fumarate), an investigational treatment for

persistent asthma in patients 12 years of age and older.

The communication, known as a 74-day letter, confirms, as

previously announced, that the NDA is sufficiently complete to permit

a substantive review and, in line with standard review practice, the

FDA has given preliminary notice of some potential review issues. The

FDA states that its filing review is only a preliminary evaluation of

the application and is not indicative of deficiencies that may

be identified during its review and that issues may

be added, deleted, expanded upon, or modified as it reviews the application.

Further clarification is required of some of these potential

review issues and steps are being taken to seek discussions with the

FDA with a view to agreeing how they may be addressed. Although the

requirements cannot be precisely assessed prior to discussion with

the FDA, based on a preliminary assessment, it appears likely that

some additional clinical work may be required to

provide more data on dosing.

As previously announced, the regulatory review timeline for asthma

treatments is typically longer than the standard 10-month

Prescription Drug User Fee Act timeline. Should

additional clinical work be required this is likely to impact

on the timeline for the review and any potential approval.

The potential review issues are not expected to have an impact

upon the development of Flutiform* for Europe or Japan. |

|

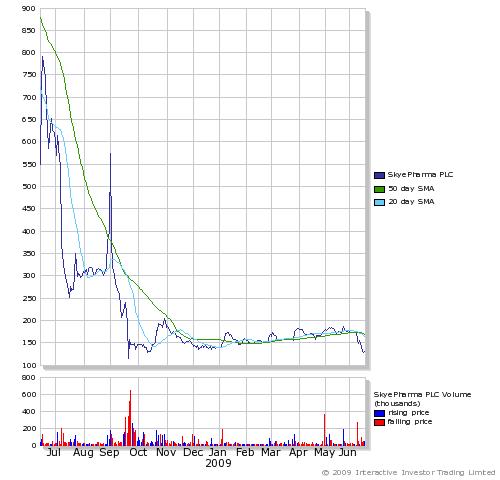

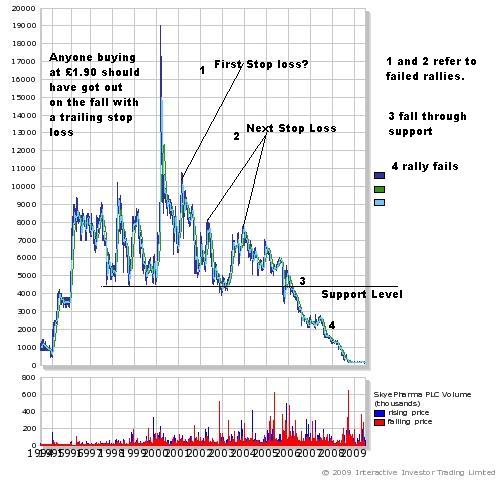

This (below) is

the chart from the company flotation - Share prices crudely converted

- no account of the number of shares in issue at the time. In my

opinion it is misleading! There are currently 23,943,162 shares in

issue - a market cap of almost £28M . At £190.00 that would

give a market cap of over $4 Billion! |

|

For buyers at

the top who failed to get out on the drop, there was a stop loss at

about £105.00 (the failed second peak) Then possibly at

£80.00 and between £60.00 amd £40.00 as the chart

recovery faltered. A more recent chart is needed to carry this forward. |

|

|

|

This was one of

my posts at iii. July 5th. - un edited.

Well if you had

bought on the top of that spike would you still hold? Look at the

graph (don't think I can add it to this reply). I WAS holding stock

prior to that peak and did NOT buy on it!

Do you

realistically consider that the "consolidated" shares can

reach £199,00? That is impossible under any management - unless

you think Flutiform is worth a market cap of

£4Billion!(£199.00 * number of shares in issue). Perhaps

around £3.00 Share price when Flutiform goes on the market.

I did not use

leverage to average down. They are fully paid for. What I might have

done, (had Barclays used the system) was take out a traditional

"call" option to buy at the current price, (114p) with a 3

month life. I'm not sure if those are still available these days, but

I did use them years ago. The price to pay was about 10% of the share

value - so it had to rise more than that to make the option

profitable. If it did go to profit you would exercise the option and

sell the stock - otherwise write off the 10% as a loss by not

exercising the option.

So if the

option cost 20pps the shares would need to be above 135p to make a

profit. At present (July24th) the option is in loss. A start price at

par (100p, costing about 15pps) was possible yesterday. |

|

Note that many sites are quoting price change as on the last

trade. This tends to produce extremes when the spread is wide, and it

can be 10% in this stock! It is often possible to trade closer to the

mid price. If, for instance the share closes at "bid" and

opens at "offer" the change displayed actually reflects the

spread! The mid price is often the same! |

|

July 6th - 12500 Buys -5045 Sells - Close price 113.5 (last deal,

not the mid!) |

|

July 7th - Initial markup very likely! No trades on main market.

Mostly buys on Plus 115.5 |

|

July 8th - More trading today buys up to 120.5 Buys 35518 Sells

71825 (not inc Plus) |

|

July 9th - Lower volume wide intra day range. |

|

July 16th - Big broker to broker trade! (see annotation on second

to last chart). 2 sells 1 buy (last) last deal 114.5. |

|

July 20th - 20 late buys of 1000 at 109.5p! Best buy at 108p

(2500). Last trade a sell at 105 sets "close" price

(105/110) Mid price then 107.5! 4 sells in all! (ADVFN data).

News re HMBioventures holding. |

|

July 21st - Suggest there will be a rally.

Mixed trading - marginally down |

|

July 22nd - first trade a sell. Spread still

wide at near 10%. It has been notable this week that when the

buy price drops and the spread narrows, buyers emerge. This

indeed did happen today. Whether this will keep the stock

above par value remains to be seen. The sell fell

to 98p but the buy remained just above par (my buy limit price).

This may be the nadir of the chart - except for a possible 96p

September last which does not show up on all charts for some reason! |

|

July 23rd. "Something4me" suggested selling - as the

company has "shafted" investors again. (FDA actually) We

shall see. Place your bets! There has again been considerably more

trading on Plus than LSE and my limit order activated. 96p was

touched and seemingly bounced off, creating a "hammer"

apparently. AR on iii has noted that, and states that all indicators

are turning up! Closed at all time low mid price of 98.75, which was

my last buy price! |

|

July 24th. If AR is right there should be some positive movement.

Indeed there was, after a weak morning. My buy yesterday cut my paper

loss by 1% and it is now showing better than break even (before

costs). As for Mr Smith?

More of these things for me!! |

|

July 27th. A strong start today on Plus led

to a 5%+ gain on the day on the LSE. Volumes were not particularly

high though.Remains to be seen if the iii poster and I who bought

have made a good call |

|

July 28th. More trades again on Plus, despite the much wider

spread there (109-123). Volumes were stronger though over 60000 in

total. Gain 5.5% today - Profit taking would seem to be the next move. |

|

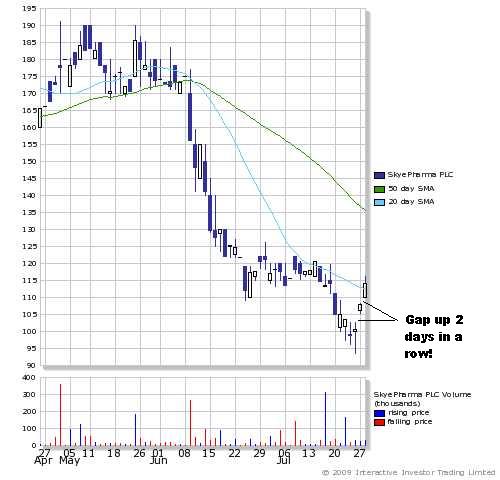

July 29th. A third opening "Gap up" in 3 days, with a

new high for this run, Volume up as well, with spread under 1p at

times! A gain of 4.3% at the close |

|

|

|

July 30th. Possible RNS today - on the back of AstraZeneca report.

Might also explain some of the rise. No RNS - think I'm wrong re AZ

connection in any case. Hardly any trading on either market today and

a widening closing spread. Last Auction trade dropped the price - Gap

down this time! Closed on the 20 day moving average! |

|

July 31st. Spread 110 - 119 at open (113.5 trade). little volume.

Shares remained unchanged. |

|

Aug 3rd. Slow start (wide spread) more larer as spread narrowed.

Gain on the day. More +ve Tech on iii. |

|

Aug 28th. The share price has passed above the 50 day sma and both

are trending up. |

|

The trends mentioed above did not hold. |

|

|

The following are from the last interim statement. |

|

As at 30 June 2008 SkyePharma had cash and cash equivalents, net

of overdrafts, of £21.3 million (31 December 2007: £31.7

million) and total liquidity (cash and cash equivalents plus undrawn

facilities) of £22.8 million (31 December 2007: £33.1

million). The decrease in cash and cash

equivalents is primarily due to the expenditure on the continued

development of Flutiform™. |

|

The pre-exceptional operating loss of £2.2 million was 75

per cent. lower than the operating loss for the

Continuing Operations recorded in the first half of 2007. The loss

was after charging £10.6 million (2007: £13.8 million) on

research and development, mainly on the continuing development of

Flutiform™. After net finance costs, the Group incurred a loss

before tax and exceptional items of £4.0 million (2007:

£14.1 million). |

|

All of the above ( middle panel) indicated better prospects for

the company as progress was indicated in the interim document in

trading in products other than Paxil CR where generic competition had

reduced revenues as expected. Whether in current trading conditions

this trend is ongoing remains to be seen - hence my opinion that the

Open Offer was very well timed! Karl Smith? Well obviously! |

|

Comparator group Re Director remuneration etc

The UK based comparator group for remuneration benchmarking consists

of fully listed and AIM quoted

Pharmaceutical and Biotechnology Companies. For 2008 the comparator

group consisted of the following companies

which were selected on the basis of industry, size (market

capitalisation, turnover and employees) and listing

environment. |

|

Abcam PLC |

Acambis Plc* |

Alizyme Plc |

|

Antisoma Plc |

Axis-Shield Plc |

BBI Holdings PLC* |

|

BTG PLC |

Dechra Pharmaceuticals Plc |

Genus Plc |

|

Goldshield Group Plc |

GWPharmaceuticals PLC |

Oxford Biomedica Plc |

|

Premier Research Group PLC* |

ProStrakan Group plc |

Protherics Plc* |

|

Silence Therapeutics PLC |

Vectura Group PLC |

Vernalis PLC |

|

* These companies were acquired during the year.

It is the intention of the Remuneration Committee to use the same

comparator group for 2009 as far as possible

(subject to changes in their status, e.g. merger, acquisition,

delisting as detailed above). |

|

Regarding a comment re the non-merger with Innovata.13-Jan-2006

Innovata has backed out of discussions for the possible "all-share"

takeover of beleaguered drug development company SkyePharma, citing

its inability to be competitive with cash-based offers from other companies.

Following the news, SkyePharma has announced that it will continue to

pursue discussions with other parties regarding potential cash offers

for the business as a whole, but had not yet received an offer it

felt could be recommended to shareholders. |

|

The boards of Vectura and Innovata are pleased to announce that, at a

Court Hearing held earlier today, the Court sanctioned the Scheme of

Arrangement and confirmed the related Reduction of Capital comprised

within the Scheme. The Scheme is expected to become effective and the

Acquisition of Innovata completed on registration of the Reduction of

Capital by the Registrar of Companies and delivery to him of an

office copy of the Court Order. This is now expected to take place on

17 January 2007.

Dealings in the New Vectura Shares issued to Innovata Shareholders

pursuant to the Scheme are therefore expected to commence at 8:00

a.m. on 18 January 2007. 17 January 2007 will be the last day of

dealings in Innovata Shares and it is expected that the Innovata

Shares will be delisted at 8:00 a.m. on 18 January 2007. |

|

Entered for consultation by those who think SKP are overpaying

directors (Annual report 2008.) |