![]()

![]()

![]()

![]()

Page details. The linked page has shareprice links too.

This page will contain the text of the preliminary results for the Year ending 31st. December 2000.

Company logo appears from the home webpage.

![]()

Mail details see the foot of this page

|

|

|

|

|

Page details. The linked page has shareprice links too. This page will contain the text of the preliminary results for the Year ending 31st. December 2000. Company logo appears from the home webpage.

Mail details see the foot of this page |

|

April 27th. Results Now available. China Review is on a separate page. See Link. |

|

AGM 30 slide Powerpoint presentation available from the company or Forest Hill. |

|

Fortune Oil PLC - Final Results RNS Number:7588C Fortune Oil PLC 27 April 2001 |

FORTUNE OIL PLC Announcement of Preliminary Results For Year Ended 31 December 2000 Fortune Oil PLC ("Fortune Oil" or "the Company"), the UK quoted company whichis involved in oil-related operations and investments in China, today announces its preliminary results for the year ended 31 December 2000. KEY POINTS * Turnover of £94.4 million (1999: £99.4 million) * Retained profit for the year of £1.3 million **(1999: £6.4 million) * Core Single Point Mooring ("SPM") project performed strongly * West Zhuhai Oil Products Terminal recorded first profitable year of operation * Trading operations affected by restructuring and by more conservative approach to business in volatile market conditions * Retail network sold to CNPC for £3.8 million 27 April 2001 **(note 1999 accounts included debt recovery of £7,377,000.)

|

||||||||||

|

CHAIRMAN'S STATEMENT |

FORTUNE OIL PLC PRELIMINARY RESULTS FOR YEAR ENDED 31 DECEMBER 2000 CHAIRMAN'S STATEMENT Introduction The year 2000 was one of consolidation for Fortune Oil, as we continued to restructure operations, improve our cost structure, and expand our infrastructure investments. Net profit for the year was 1,333,000 (US$2,028,000), against a profit of 6,373,000 the year before. The Single Point Mooring (SPM) facility performed especially well. With continued growth in energy demand in China, we expect a solid performance in 2001. Restructuring and Debt Recovery The restructuring process we launched in 1999 continued to bring results. During 2000, we disposed of our petrol station network in China at an acceptable valuation, using the proceeds to reduce debt. Much effort was devoted to resolving the disputes connected with the earlier restructuring of our trading business and we are confident that all matters outstanding will be settled during the current year. Fortune Oil should benefit from any settlement. It will also allow us to resume fully our trading operations. The restructuring process is now largely completed and we have made full provision for all costs. Our success during the year in net recovering 0.7 million (US$1.1 million) in debt we had written off from trade debtors contributed to company profits. We will continue to pursue claims vigorously, which will support our bottom line. Operations Our core businesses again performed well. The SPM set a new record, with throughput rising 63 per cent over 1999 to 8.4 million tonnes. This resulted in a 62 per cent rise in earnings from the unit to 7.8 million (US$11.8). Sales volumes at Bluesky rose 7.5 per cent but profits only reached 0.4 million (US$0.6 million). The Bluesky performance was achieved in difficult operating conditions, as the approvals process in China made it impossible for us to immediately pass on increases in jet fuel costs to customers. Our strict controls on operating costs and capital expenditure were central to our ability to achieve good returns and demonstrate the Company's competitiveness in the China aviation fuel market. Turnover at our trading operation was below expectations and this was the main reason for the fall in overall revenues. Rising levels of volatility were not conducive to higher levels of trading activity at acceptable levels of risk. We were also constrained by the disputes surrounding the restructuring of this operation. Management Mr. Richard Wong left the post of Joint Chief Executive Officer on 16th April 2001. It is the Board's intention in the short term to appoint a new executive director and Ms. Li Ching, Joint Chief Executive Officer, will carry out Mr. Wong's duties, assisted by the executive management of the company. Prospects Our success in restructuring the Company has laid a solid foundation for future development that will improve during 2001. The continued growth in energy demand in China can only benefit our core businesses. Our intention is to identify and develop additional infrastructure projects and businesses associated with oil and petrochemicals where we can make use of the experience and expertise that we have gained in our operations in China. As a leaner, more focused operation, with strong partners in one of the world's largest and fastest growing energy markets, I believe our long-term fundamentals remain attractive. Qian Benyuan Chairman 27 April, 2001 |

||||||||||

|

CHIEF EXECUTIVES' REVIEW |

I have pleasure in reporting that Fortune Oil has largely completed its restructuring activities, further consolidated its operations and made satisfactory overall progress in expanding its infrastructure investments during the period under review. REVIEW OF OPERATIONS The Single Point Mooring (SPM) facility continued to show a good return to the partners of the joint venture. The Bluesky aviation refuelling joint venture reported a profit for the year, in spite of a very severe operating environment. Following China National Petroleum Corporation (CNPC) becoming a shareholder in the West Zhuhai Oil Products Terminal in 1999, the joint venture reported its first profitable operating result this year. The Zhanjiang Fu Duo LPG facility reported a loss for the year, which was due to the extremely competitive market conditions in the area which adversely affected importers of LPG. The retail business has been sold to CNPC, with the legal documentation now complete. This further tightened our close working relationship with one of the two major oil companies in China. The trading division was further restructured during the year and, as a result, fewer than expected transactions were completed. We are also excited about the progress made towards further expansion in our infrastructure investments, which will be explained in the following sections. RESULTS The retained profit for the year is £1.3 million (US$2.0 million) (1999: £6.4 million). Total turnover decreased by 5 per cent to £94.4 million (US$143.6 million) due to the reduction in oil trading activities. Turnover for infrastructure projects increased with the Single Point Mooring and South China Bluesky Aviation Oil Company Limited continuing to be profit contributors for the Company. The West Zhuhai Oil Products Terminal also recorded its first profitable year of operation. The Zhanjiang Fu Duo LPG facility suffered a loss. INFRASTRUCTURE INVESTMENT

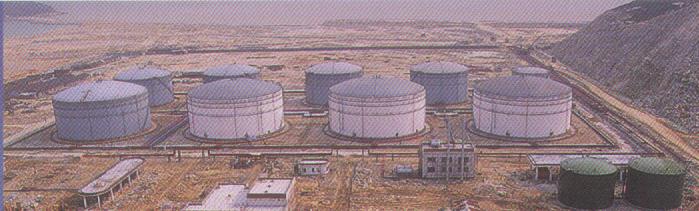

The SPM continued to set new records in its operation. During the year, with the support of Maoming Petrochemical Corporation (MPCC), 41 large-scale oil tankers discharged a record 8.4 million tonnes of crude oil at the SPM, up 63 per cent from 1999. Total revenue for the year was £14.5 million (US$22.0 million) and net profit was £7.8 million (US$11.8 million), increase of 50 per cent and 62 per cent respectively. The US$2.67 million bank loan was further reduced by US$1.33 million, leaving a balance of only US$1.34 million now outstanding. The SPM has been in operation for nearly 6 years. In the past year, we undertook a thorough inspection and maintenance of the facility, and replaced key equipment to ensure that the SPM continues to be in good working condition. The outlook for the SPM is highly promising. The Maoming refinery has the capacity to refine about 12 million tonnes of oil and has processed over 10 million tonnes of crude oil in 2000, which has made the Maoming refinery the largest in China. The Maoming refinery has also recently secured a major contract from the Central Government, under which it will supply around 10 million tonnes of oil products through pipelines to the provinces of Southwest China from 2005. Aviation Fuel Supply Joint Venture The Bluesky Aviation refuelling joint venture experienced significant challenges in its second full year of operation. After a prolonged period of high jet fuel supply costs, which it was unable to pass on to the airlines on a timely basis due to the domestic price increase approval process, the joint venture reported a profit of £0.4 million (US$0.6 million) 67% short of its budget profit of £1.2 million (US$1.9 million) by 67 per cent although sales volume increased by 7.5% per cent over 1999. The joint venture partners are currently putting together a programme working with CAAC (General Administration of Civil Aviation of China), with the objective of reforming the pricing policy to bring it more in line with the international market, ultimately creating a more efficient pricing structure. Simultaneously, the management of the joint venture continued to control operating costs as well as capital expenditure. It was this control of costs which contributed to the joint venture's profitability last year. Construction of the new Guangzhou Airport is underway and it is expected to commence operation in 2003. The new jet fuel refuelling system is progressing as planned and we expect the project to be finished within the timetable and in line with the required standards. As China's economic activity continues to grow, we are confident that this investment will provide excellent returns for its shareholders in the years to come. West Zhuhai Oil Terminal and Storage

Year 2000 proved to be a major milestone for the West Zhuhai Oil Terminal and Storage Facility as it became profitable for the first time. Throughput volume was 1.66 million tonnes, up 55% from 1.07 million tonnes in 1999. Revenues of £3.49 million (US$5.31 million) were achieved, up 65% from 1999, with £0.1 million (US$0.2 million) of profit. The move from loss to profit was as the result of three factors: first the increased throughput, second the increase in the throughput charge, up 30% from RMB20 to RMB26 per tonne, and third the strengthening of cost controls. For 2001, we expect that the throughput volume will increase to around 1.8 to 2.0 million tonnes. In addition, during their planning year 2001 and 2002, The Guangzhou branch of China National Petroleum Corporation (CNPC) is likely to increase gradually its sales volume to around 3.5 million tonnes. 70% of this will be throughput via the West Zhuhai Oil Terminal and Storage. As a result, the West Zhuhai Oil Terminal and Storage is therefore proceeding with the second phase of its development, including an additional 110,000 cubic meters of oil tanks and two new 1,000 MT-class berths. The total investment is equivalent to RMB66 million (£5.5 million), of which RMB46 million (£3.87 million) will be financed by CNPC's finance company and the rest, RMB20 million (£1.68 million), will be shared among the shareholders; Fortune's share will be RMB3.7 million (£300,000). The project is expected to be completed by early 2002. The second phase of the project will further strengthen the relationship with CNPC, our partner. Fu Duo LPG In 2000, Fu Duo experienced the worst market environment since its establishment in 1994. Fierce competition from regional refineries, coupled with very high imported supply costs, created a serious challenge to the joint venture. Average imported supply costs were substantially higher when compared to year 1999. As a result, sales volume was reduced to 67,900 tonnes, down 55 percent from 1999 and a loss of £1.2 million (US$1.8 million) was suffered forthe year. Under such difficult conditions, Fu Duo decided to respond to the challenge by changing the management and restructuring the company, reducing the number of employees, and contracting out most of the subsidiary operations. We are also working on a number of further initiatives to improve the overall performance of the joint venture, including introducing a strategic partner to raise efficiency through added synergies. In 2001, Fu Duo will be focusing on consolidation of its internal management structure, developing retail outlets, and establishing a more sophisticated trading force through co-operation with Fortune Oil Trading Company Limited, with a view to improving its overall performance. AcroChina Technology Inc. In the beginning of 2001, Fortune invested £0.1 million (US$0.2 million) to take a 51% share of a software company in China - AcroChina Technology Inc., which has taken over the business of AcroChina Inc., a software company with over 2 years operating history. AcroChina Technology's business includes the development and sales of a range of software and systems for use in the oil and gas industry as well as in the telecommunicatios industry. Its software products include a Sales System for oil and gas companies, a Depot Control and Management System for oil and gas companies, a Transportation Optimization System for oil and gas companies, a Production Analysis and Decision Making System for oil fields, and a Billing Systems for telecommunication companies. AcroChina Technology is the key independent software reseller of Oracle Corporation software in China. It sells both database and application products from Oracle. Trading Trading performed lower than expected in 2000. Turnover decreased to £31.8 million (US$48.4 million) compared to £58.0 million (US$93.7 million) in 1999. This significant decrease was due to reduced trading activities during the year, as the market conditions were quite volatile and the trading team adopted a more conservative approach to the conduct of its business, following the problems in 1998. The other reason for reduced trading was the limited availability of banking facilities during the year, as the Company has not fully re-established its trading links with banks and because of continuing disputes with certain trading partners. We expect these matters can be resolved during 2001, so that the crude oil business should grow in 2001 as the Company becomes more financially stable. Restructuring Towards the end of the year, the Company successfully sold its retail network in the Guangdong Province to CNPC for total consideration of £3.8 million (US$5.7 million). The timing of the sales worked in our favour, as there were a number of interested potential buyers in the market who all wanted to expand their market share. As a result, we were able to sell our network at minimal loss, in spite of the original high investment costs. Last year, we reported that the Company had obtained a 90 per cent interest in a Beijing hotel as collateral for settlement of an overdue account receivable. During the year, we took the balance of the interest in the hotel as settlement of the unpaid debt, as we considered that controlling the collateral and having the unfettered ability to sell it for cash was a better option. Since then, we were able to find a buyer, the Shenyang Provincial Government, to take over the hotel. A down payment of £2.5 million (US$3.7 million) was paid during the fourth quarter of the year. However, due to changes in senior personnel in the Provincial Government, the completion process has now been delayed but we hope and expect to reschedule completion shortly. Meanwhile, the hotel is running well, at an occupancy rate above 70 per cent. If, after an appropriate period of time, the deal is not complete, we have the option of keeping the deposit and seeking another buyer. We believe the hotel value continues to increase and that it is very attractive to international hotel operators as its location is prime and the facilitiesare suitable to both leisure and business travellers. Should Beijing be successful in its bid to host the 2008 Olympic Games, the hotel's value could be even higher. Litigation As mentioned earlier, the Company is involved in several lawsuits, as a result of trade disputes which took place in 1998 concerning one of our former subsidiaries. We are confident that these legal matters will be resolved favourably during 2001, so that our management can focus more on the day-to-day operation of the Company. |

||||||||||

|

The Year Ahead

|

The Year Ahead To establish a favourable platform for future development prior to China's entry into the World Trade Organisation (WTO) we intend to leverage our current situation in China by expansion and upgrading of our existing facilities and by the development of new activities which will benefit from WTO status. The major shareholders are seriously considering converting the Loan Stock into shares during this year. The Company is actively pursuing several prospects for development of new projects associated with our core competences in China which have the potential to provide a source of increased and sustained profitability in the future. 2000 was not an easy year for Fortune Oil, which encountered difficulties and pressures from many sides. Among the problems the Company faced, certain projects have proceeded less efficiently than expected, whilst sizeable borrowings have resulted in high financing costs, even as certain new projects under construction have required more capital. Nevertheless, after seven years of progress, Fortune Oil has accumulated rich experience and expertise in developing trading and infrastructure projects in China providing great potential for the company. I believe if we continue to progress and are not discouraged by the current temporary difficulties, we can continue steadily to develop Fortune Oil and realise new successes in the 21st century. Li Ching Chief Executive 27 April 2001 |

||||||||||

|

Fortune Oil PLC 4/F, Bowater House East, 68 Knightsbridge, London SW1X 7LJ, United Kingdom Tel: 020 7589 2233 Fax: 020 7589 7755

Suite 2801, 28th Floor, Great Eagle Centre, 23 Harbour Road, Wanchai, Hong Kong Tel: 2802 8300 Fax: 2802 8322

|

|||||||||||

|

Page compiled 24th April 2001 revised April 2001, June 2001 |