|

One company worth a close look is London-based drug delivery group

SkyePharma Plc, which is on the threshold of achieving maturity and

offers considerable growth potential. The good news is that the

shares (SKYE: news, chart, profile) are still reasonably cheap and

have yet to attract a glamour rating enjoyed by so many "jam

tomorrow" businesses in the US.

But perceptions are likely to change as its 2002 results, due within

a month, and a patent issue, remove some of the uncertainty

overhanging the stock.

SkyePharma develops novel devices and processes to improve the way

existing medicines are administered to patients. As a result, it

starts off with an advantage over pure biotech companies, which face

a considerable risk that a brand-new concoction made in the lab after

years of expensive research fails to get past regulatory hurdles.

The group's proprietary technology is of potential value to many drug

companies that either want to extend the patent life of their

existing drugs by adopting a new method of delivery, or to simply

improve the quality of treatment to patients. In return, SkyePharma

receives license payments as well as on-going royalties linked to

future sales of a drug.

The group has expertise in a wide range of methods of delivery. It

can make pills dissolve more slowly, once swallowed, so that the drug

works over a longer period. It can enable inhalers to work better so

that powdered-drugs they contain don't congeal with moist breath. Or

it can add a magic ingredient to an injection-delivered drug so that

patients need fewer jabs - a great boon for the many millions who

hate needles!

Not surprisingly, SkyePharma has commercial tie-ups with many drug

majors including GlaxoSmithKline (GSK: news, chart, profile) and

Novartis (NVS: news, chart, profile), which are applying its

technology to launch new versions of their big selling drugs.

The group has about a dozen projects for new drugs or approved

products on the market. That means it is now poised to transform from

a development stage company into a profitable business with growing

revenue streams, starting this year.

The big breakthrough is likely to come from Paxil CR, a faster-acting

version of Glaxo's blockbuster anti-depression drug. This drug has

been on sale since last year and U.S. doctors seem to like the newer

version. It now accounts for 32 percent of all new prescriptions

written for Paxil, suggesting that the newer version itself could

become a $1 billion a year drug.

SkyePharma gets a 3 percent royalty on Paxil CR sales, a small slice

from a mega-sized cake. On the other hand, the group is entitled to

fatter slices of royalties from its family of injectible painkillers

through its joint ventures with U.S.-based Enzon (which is planning a

merger with NPS Pharmaceuticals) and Endo. The royalty rate for one,

DepoMorphine, a post-operative painkiller, could be as high as 60

percent subject to sales targets being achieved. Developed by

SkyePharma, it is supposed to be filed for approval with the FDA

later this year.

Peter Laing, corporate communications director at SkyePharma, said

"This product has huge potential for us and could become more

important than Paxil CR. It is being described as revolutionary in

some circles."

Other exciting products on the way include a long-acting respiratory

drug, Foradil, owned by Swiss giant Novartis. The new version was

filed with the FDA last December and could be on the market by late

this year.

Meantime, expect positive news soon from SkyePharma's novel cream for pre-cancerous

skin ailments caused by too much sun. The product, Solaraze, was

approved for sale a year ago, but is only now gaining momentum after

SkyePharma relicensed marketing rights to Quintiles in the US and

Britain's Shire Pharmaceuticals in Europe and Australia.

SkyePharma's late-stage product pipeline means the group is expected

to move into profits this year. However, the shares have yet to catch

the limelight. One reason is that Glaxo's original patent on Paxil is

being challenged by generic drug makers in U.S. courts within a few

weeks. While the case does not directly affect Paxil CR, the newer

version, Laing concedes that it may have some knock-on effect on its

future sales potential.

Even so, the upside potential for SkyePharma is much greater than the

downside risk for long-term investors. At a guess, the odds of Glaxo

winning its case are more than even. Victory could also be a big

boost for SkyePharma and perhaps help to double its share price over

the next 12 months. Lose, and the shares could easily halve.

Another drag on the share price is that the group will remain heavily

reliant on one-off payments from deal making until royalty streams

build up over the next few years.

Still, investors are likely to gain more confidence once it reports

its 2002 results. Some British investors want to be see it deliver on

its promise to report a significant profit for the year. That will

depend on whether it can book a $25 million license payment from Endo

in last year's results or this year.

But this has become an issue tied-up in emotion. What matters more is

that the money is already in SkyePharma's bank account and has helped

to swell its estimated cash balances to about a $100 million. The

group was also cash flow neutral in the first half and a full year

profit of any size should warm investor sentiment.

Valuing SkyePharma is still dependent on forecasting future sales of

drugs. However, on current market estimates the group should move

into profits of about 6 million British pounds in 2002 and surge

five-fold by 2004 as new products hit drug stores. Group revenues are

expected to triple from a reported 46 million in 2001.

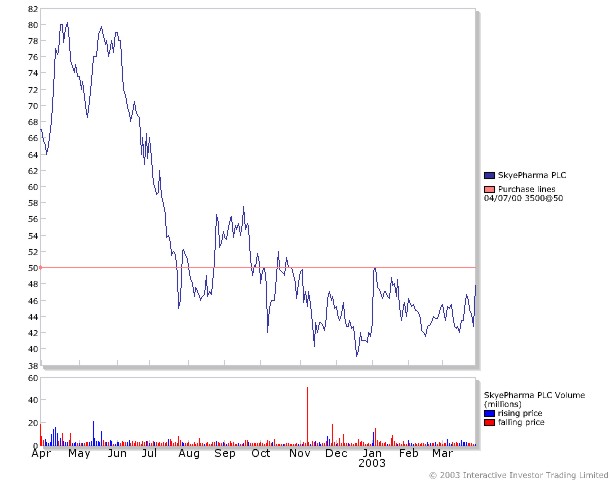

At 45 pence a share in Britain, or $7.09 for Nasdaq-listed shares,

the stock is valued at about 17 times expected earnings for this year

-- appealing for the risk tolerant investors looking for a high

reward/high risk play. |